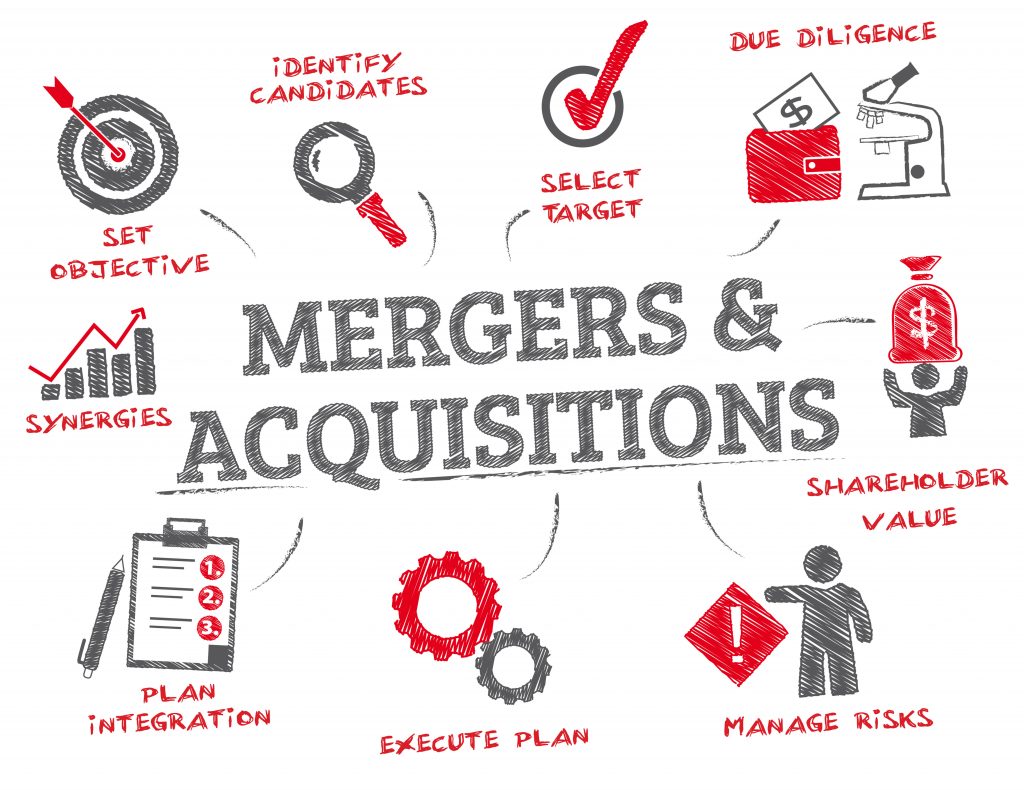

Mergers & Acquisitions

RwE has been providing selective M&A support services for many years.

We understand the profession and are well connected, reasonable and respected.

We visit hundreds of firms each year and over time, we have developed very close working relationships with a large number of them.

In many instances, these firms talk to us about their future intentions, so we’re best placed to put like-minded buyers and sellers together.

We also have contact with hundreds of firms through our valuation and financial consultancy work. This network of firms means we’re ideally placed to be told about the owners’ future intentions.

Furthermore, our fees for providing M&A services and introductions are highly competitive, making the buying or selling of practices a little bit easier to swallow. Let us help you.

What we have found is that the dominant rationale used to explain M&A activity is that acquiring firms seek improved financial performance.

The following motives are considered to improve financial performance:

- Synergy: This refers to the fact that the combined company can often reduce its fixed costs by removing duplicate departments or operations, lowering the costs of the company relative to the same revenue stream, thus increasing profit margins.

- Increased revenue or market share: This assumes that the buyer will be absorbing a major competitor and thus increase its market power (by capturing increased market share) to set prices.

- Cross-selling: For example, a bank buying a stock broker could then sell its banking products to the stock broker’s customers, while the broker can sign up the bank’s customers for brokerage accounts. Or, a manufacturer can acquire and sell complementary products.

- Economy of scale: For example, managerial economies such as the increased opportunity of managerial specialization. Another example are purchasing economies due to increased order size and associated bulk-buying discounts.

- Taxation: A profitable company can buy a loss maker to use the target’s loss as their advantage by reducing their tax liability. In the United States and many other countries, rules are in place to limit the ability of profitable companies to “shop” for loss making companies, limiting the tax motive of an acquiring company.

- Geographical or other diversification: This is designed to smooth the earnings results of a company, which over the long term smoothens the stock price of a company, giving conservative investors more confidence in investing in the company. However, this does not always deliver value to shareholders (see below).

- Resource transfer: resources are unevenly distributed across firms (Barney, 1991) and the interaction of target and acquiring firm resources can create value through either overcoming information asymmetry or by combining scarce resources.

- Vertical integration: Vertical integration occurs when an upstream and downstream firm merge (or one acquires the other). There are several reasons for this to occur. One reason is to internalize an externality problem.

However, on average and across the most commonly studied variables, acquiring firms’ financial performance does not positively change as a function of their acquisition activity.

Therefore, additional motives for merger and acquisitions that may not add shareholder value include:

- Diversification: While this may hedge a company against a downturn in an individual industry it fails to deliver value, since it is possible for individual shareholders to achieve the same hedge by diversifying their portfolios at a much lower cost than those associated with a merger.

- Manager’s hubris: manager’s overconfidence about expected synergies from M&A which results in overpayment for the target company.

- Empire-building: Managers have larger companies to manage and hence more power.

- Manager’s compensation: In the past, certain executive management teams had their payout based on the total amount of profit of the company, instead of the profit per share, which would give the team a perverse incentive to buy companies to increase the total profit while decreasing the profit per share (which hurts the owners of the company, the shareholders); although some empirical studies show that compensation is linked to profitability rather than mere profits of the company.